Negotiations, delays, and revisions marked the Corporate Sustainability Due Diligence Directive (also known as the "CSDDD" or the "CS3D"), which was approved by the European Parliament with revised text on April 24, 2024. This signaled a significant shift in corporate responsibility across the EU. Currently, EU lawmakers are negotiating the final text of the CSDDD in trilogues and are expected to reach an agreement in early 2024.

In this blog post, we will examine the significant revisions made in the final text of CS3D, with a particular emphasis on critical aspects like Scopes, Reporting Obligations for Due Diligence, and the Influence of CS3D on Scope 3 Emissions.

A Closer Look at CS3D's Final Text

While the exact thresholds for the CSDDD's application are still under consideration, one of the most notable changes in the finalized version of the Corporate Sustainability Due Diligence Directive (CSDDD) is its significantly narrowed scope.

EU-based and non-EU companies operating within the EU market will be subject to specific criteria regarding employees and turnover. However, the application thresholds have substantially increased, reducing the number of companies within its purview.

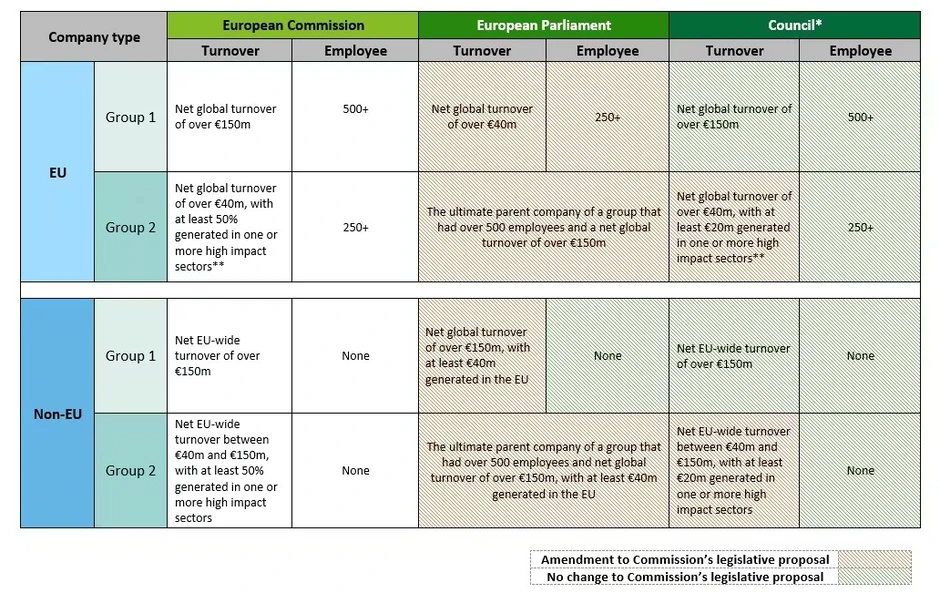

According to Deloitte's table, the new directive is likely to encompass two main groups:

-

Large EU companies: Those with a global turnover exceeding €150 million and employing over 500 individuals.

-

Large non-EU companies: Those whose EU-wide revenue surpasses €150 million.

Source: Deloitte

Source: Deloitte

EU Companies

Initially, the directive targeted companies with 500 or more employees and a net turnover of 150 million euros. However, after deliberations, these thresholds were increased to 1,000 employees and a turnover of 450 million euros. This adjustment means that the directive will now affect approximately 0.05% of businesses operating within the EU.

Furthermore, EU companies with over 250 employees and a global turnover exceeding €40 million will also come within the directive's scope if at least half of their turnover is derived from high-risk sectors. As outlined by the directive, these sectors include the manufacturing of textiles, leather, related products, agriculture, forestry, and fisheries, as well as the extraction and manufacturing of mineral products.

Non-EU Companies

The criteria for non-EU companies are slightly less defined. However, EU-based companies operating in high-risk sectors with a global turnover surpassing €40 million and employing over 250 individuals should anticipate compliance requirements. Similarly, non-EU companies operating within these sectors in the EU market, with an EU-wide turnover exceeding €40 million, will likely fall under the directive's purview.

While the CSDDD's scope may have narrowed, its impact is poised to be more concentrated and effective. It will target key players in the corporate landscape and drive meaningful progress toward sustainable and responsible business practices within the EU.

CSDDD & CSRD Reporting Alignment

In terms of reporting, even if compliance with CSRD's reporting obligations exempts companies from specific reporting under the CS3D, companies covered by the CS3D without CSRD obligations must publish an annual statement on their website. This statement should cover CS3D requirements and be published in EU official or internationally customary languages within one year of the financial year-end.

By March 31, 2026, the Commission will establish clear reporting guidelines to provide a standard framework for communication practices and enhance consistency and transparency. This includes specifying due diligence descriptions, identifying environmental and human rights impacts, and detailing mitigation measures. Comprehensive requirements are expected, comparable to CSRD reporting, possibly including mandatory questionnaires similar to those under national legislation like the German Supply Chain Act.

The forthcoming CS3D reporting requirements present a unique opportunity for companies to proactively integrate Scope 3 emissions disclosures within their broader sustainability reporting frameworks. By aligning due diligence efforts with Scope 3 emissions mitigation strategies, companies can demonstrate a comprehensive approach to addressing environmental and social impacts throughout their value chains. This integrated approach empowers companies to promote transparency and accountability while driving progress towards sustainability goals.

High-Accuracy GHG Emission Reporting

The Impact of CSDDD on Scope 3 Emissions Reduction

To better understand how this directive relates to Scope 3 transportation emissions, it's essential to recognize the broader context of corporate responsibility. Scope 3 emissions refer to indirect emissions generated from sources not owned or controlled by the reporting organization but associated with its activities, including emissions from transportation, distribution, and the use of products or services.

How can the CS3D directive be understood within the context of Scope 3 Transportation emissions?

1. Supply Chain Accountability: The CS3D mandates companies to examine and document findings not only within their immediate operations but also across their supply chains, both upstream and downstream. By addressing environmental impacts throughout their value chains, companies are indirectly required to consider and mitigate Scope 3 transportation emissions.

2. Due Diligence Requirements: The directive necessitates a thorough due diligence process that includes identification, assessment, prevention, and mitigation of adverse environmental impacts. This encompasses elements like emissions and pollution directly relevant to transportation activities. Companies must assess how transportation-related activities contribute to their overall environmental impact and take measures to minimize these emissions.

3. Contractual Obligations to Suppliers: The CS3D indirectly affects smaller companies operating in the value chains of larger corporations through contractual requirements imposed on them. If transportation activities contribute significantly to a company's Scope 3 emissions, they would be expected to address these concerns as part of their contractual obligations to larger entities, thereby indirectly impacting transportation practices and emissions.

Although CS3D might primarily target environmental and human rights issues within corporate operations and supply chains, its requirements for due diligence, supply chain accountability, and contractual obligations can indirectly influence companies to address Scope 3 transportation emissions as part of their broader sustainability efforts. Except for the scopes, obligations, and penalties for non-compliance, this pivotal initiative also sets the right global foundations regarding environmental, social, and governance (ESG) issues, promoting sustainable and responsible corporate behavior through both the company's operations and its governance.

To identify and mitigate adverse environmental impacts, assess the effectiveness of emission reduction efforts, and transparently change their direction, companies should abandon average calculation methods that use historical data and conversion factors and seek solutions and partners that utilize technology and primary data to provide them an accurate and holistic picture of their environmental footprint.